Call Our Office

(559) 384-2900 | Fresno

(619) 480-1413 | San Diego

(619) 480-1413 | San Diego

Your Money

Your Life

Your Way

You are now leaving the Strong Valley Wealth & Pension, LLC ("Strong Valley") website. By clicking on the "Schwab Alliance Access" link below you will be entering the Charles Schwab & Co., Inc. (“Schwab”) Website. Schwab is a registered broker-dealer, and is not affiliated with Strong Valley or any advisor(s) whose name(s) appears on this Website. Strong Valley is/are independently owned and operated. Schwab neither endorses nor recommends Strong Valley. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Strong Valley under which Schwab provides Strong Valley with services related to your account. Schwab does not review the Strong Valley website(s), and makes no representation regarding the content of the Website(s). The information contained in the Strong Valley website should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.

Saint Agnes Men's Club is a dynamic group of philanthropic men, whose fundraising efforts have benefited the Medical Center and its special programs since 1983. Since its inception, Saint Agnes Men's Club members have generated more than $3.8 million to support Saint Agnes patient care services and community outreach programs.

Since 1929, Saint Agnes Medical Center has been known for delivering high quality, compassionate care to meet Central California’s growing and diverse health care needs.

Each dollar raised goes to support many Saint Agnes programs and services that benefit our community. Some include (but not limited to):

Strong Valley was pleased to support the recent Saint Agnes Men’s Club Golf Tournament fundraiser by sponsoring a hole for the longest drive. It was a great time for all as well as a successful source of finances for a very worthy organization.

“Overall economic activity appears to have picked up after edging down in the first quarter. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher energy prices, and broader price pressures.

The invasion of Ukraine by Russia is causing tremendous human and economic hardship. The invasion and related events are creating additional upward pressure on inflation and are weighing on global economic activity. In addition, COVID-related lockdowns in China are likely to exacerbate supply chain disruptions. The Committee is highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 1‑1/2 to 1-3/4 percent and anticipates that ongoing increases in the target range will be appropriate. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in the Plans for Reducing the Size of the Federal Reserve's Balance Sheet that were issued in May. The Committee is strongly committed to returning inflation to its 2 percent objective.”

From the Federal Reserve press release dated June 15, 2022.

This rate hike – as the previous hike earlier this year – was one of the most predictable and predicted rate movement the markets have ever seen. What was not predicted until recently, however, was the magnitude of the rate hike.

Yet while the markets and traders were expecting this hike, the announcement did contribute to the DJIA, NASDAQ and the S&P 500 all rallying by more than 1%. But within a few hours after markets closed, the futures market suggested that those gains would be wiped out the following day.

Keep in mind that’s only one trading day and one futures “night” – long-term investors should think about the risk that the Fed continues moving rates higher and faster than expected throughout 2022, because then we could see some longer-term challenges for the stock market and consumers. And higher rates are all but certain to happen for the remainder of the year. The magnitude, however, depends on a number of factors.

“Clearly, today’s 75 basis point increase is an unusually large one, and I do not expect moves of this size to be common,” said Fed Chair Jerome Powell. And Powell also said that decisions will be made “meeting by meeting.”

Interestingly, as of the day after the Fed’s historic announcement, Wall Street assigned a probability of more than 80% that the Fed would raise rates by another 75 basis points at their next meeting at the end of July.

So, will there be implications of this announcement? Sure. But enough to make most investors change allocations or courses of action? Maybe. Maybe not.

The most important tool available to the Fed is its ability to set the federal funds rate, or the prime interest rate. This is the interest paid by banks to borrow money from the Federal Reserve Bank. Interest is, basically, the cost to the banks of borrowing someone else’s money. The banks will pass on this cost to their own borrowers.

Increasing the federal funds rate reduces the supply of money by making it more expensive to obtain. Reducing the amount of money in circulation, by decreasing consumer and business spending, helps to reduce inflation.

Any increased expense for banks to borrow money has a ripple effect, which influences both individuals and businesses in their costs and plans.

These broad interactions can play out in numerous ways.

This one is a bit trickier because intuitively stock prices should decrease when investors see companies reduce growth spending or make less profit. The reality, however, is that the Fed typically won’t raise rates unless they deem the economy healthy enough to withstand what should – at least in textbooks – slow the economy. But the reality is that stocks often do well in the year following an initial rate hike. But after multiple and large rate hikes in the same year? Much tougher to predict.

If the stock market declines, investors tend to view the risk of stock investments as outweighing the rewards and they will often move toward the safer bonds and Treasury bills. As a result, bond interest rates will rise, and investors will likely earn more from bonds.

Obviously, many factors affect activity in various parts of the economy. A change in interest rates, although important, is just one of those factors.

Call us if you have questions or want to discuss additional repercussions that this Fed rate increase will likely have.

Waking up early in the morning before the sun is up and heading to the gym comes hard. Once your workout ends, though, you often begin the day with the payoff of a tremendous energy boost. Can the same process apply to your finances?

If you’re like most people, you exercise for many reasons but expect to benefit from your sweat equity in the future, not in the current moment. We will all encounter health issues at some time and the medical world assures us that we’ll deal better with problems if we get – and stay – physically fit. Preparation matters.

What does exercise have in common with financial planning and investing? The answer: Very few individuals prepare to invest, except maybe when selecting from choices in a retirement plan.

Or not: Studies showed that even in the teeth of the Great Recession and perhaps the most volatile market year in history – most 401(k) retirement plan participants made no changes to their contributions.

Getting back to the fitness analogy, exercise’s greatest benefits come from the stress we intentionally place on our muscles so that when a health problem arises, our bodies are in better condition to deal with the situation. Regarding investments, you need a methodical (and regularly visited) regimen for taking in and processing market data. You also need a strategy to accommodate unforeseen yet inevitable future events, such as market downturns.

Don’t let random financial news clips guide your decisions. Filter out market noise when determining how to act. For the record, you need not re-allocate asset classes or otherwise change your portfolio just because something in the market changed. You do need to be prepared to consider adjustments when the information dictates that conditions shifted, such as stocks increasing to a higher portion of your portfolio than you want.

Financial advisors call this as an investment policy statement. Or you might prefer the term “investment playbook.” The playbook outlines your holdings and specifies how you intend to respond to change with a disciplined approach aimed at particular objectives – as opposed to the usually heated emotions most of us feel in a suddenly rough market.

How are your holdings doing against benchmarks such as the Standard & Poor’s 500 Index? At specifically what point will market shifts make you re-allocate percentages of stocks and bonds in your portfolio?

Your playbook also describes what you’re trying to achieve as an investor – pay for retirement or for college tuition, for example – and how you’ll react to market changes. You might plan to sell or buy only if the S&P 500 hits a certain number or invest in oil if the cost per barrel drops to a pre-set price. A well-designed playbook keeps you from panicky decisions or from freezing up during Wall Street roller coasters.

Your playbook needs to clearly document your investment information sources, the technology involved in your investing and why you bought a particular investment.

Remember: Great stock or mutual fund opportunities may arise and shimmer, but if they don’t match your playbook, you pass.

At the gym, you can wander among the clanking weights or plan exactly how to invest your energy. You know which method works better.

Investing is no different.

Talking with a financial advisor can help you get into a consistent financial fitness plan for your unique situation.

Sometimes we forget just how fragile a nest egg can be.

When the economy tanked in 2008, retirees watched in horror as U.S. markets suffered historic losses. The Dow declined by more than 50%, its biggest drop since the Great Depression of 1929.

The oldest Baby Boomers, who were closing in on retirement age just as things were at their worst, watched as their nest eggs cracked wide open and lost thousands of dollars – in some cases hundreds of thousands.

Most were left with two choices: Either keep working past the age they'd planned to retire (Boomers started turning 65 in 2011) or retire with a lifestyle that was substantially downsized from what they once had envisioned.

Under both scenarios, they could struggle to piece back together the plans they once had. But we all know how that goes. Time was not on their side.

Pre-retirement is one of the worst times to experience significant market loss, because there is often little time left for recovery. You need that nest egg you accumulated to generate income when the paychecks stop. If it shrinks, so will the amount of income you'll get.

That's why financial professionals talk so much about volatility and why you should start pulling back from risk as you get older. The markets will always move up and down. And given today's uncertainty -- both domestic and worldwide -- some loss seems almost unavoidable.

But there are distribution strategies that can help give you an edge in overcoming a loss.

For the average retiree, one way to help distribute retirement income is not by putting hope in the market, but by using an actuarial-designed product, such as an annuity. With an annuity, distribution amounts are, in large part, calculated based on your age and life expectancy; the older you are, the more you get paid.

Let's say you know a 70-year-old man who had a portfolio worth $500,000. He expected to generate about 3% in retirement income – about $15,000 per year.

But then he suffered through a serious market downturn, and his $500,000 portfolio was reduced to $300,000. At that 3% withdrawal rate, his annual income would decline drastically. In order to replicate the $15,000 per year he planned to pull from his portfolio, he would need to invest aggressively – meaning more risk and a greater chance of losing even more money.

Now, instead, let's say your friend purchased an immediate annuity with an A+ rated carrier. With a deposit of $209,375, he could generate the $15,000 per year in lifetime income he'd originally planned on. His purchase would be converted into regular payments that would last as long he lives. His annuity would guarantee him a 7.2% return, which could help reduce his fear of running out of money in retirement.*

Using an annuity to distribute income is a way to overcome market losses -- or to avoid them altogether. And it can offer you the confidence that you will be able to enjoy your well-earned retirement through protection of the principal and regular income streams.

It is important to remember annuities do have surrender charges, making them a non-liquid asset. Additionally, annuities do have fees and can limit your ability to participate in market gains, even with products such as fixed index annuities. However, some retirees enjoy the comfort of the steady income and the protection benefits offered by annuities.

Most traditional immediate annuities are pretty straightforward once you've made the purchase. But you'll definitely want to work with a financial professional to lock down what's an appropriate product for you, and to review any changes to your goals or financial situation as you age.

*Annuity guarantees are backed by the financial strength and claims-paying ability of the issuing insurance company.

These are hypothetical examples provided for illustrative purposes only; it does not represent a real-life scenario, and should not be construed as advice designed to meet the particular needs of an individual's situation.

It's important for you to talk to your financial advisor to discuss your specific circumstances and goals.

Through the support of nearly 1 million members, Ducks Unlimited is the largest non-profit wetlands conservation organization in the world!

For 85 years, DU has conserved, restored, and managed over 15 million acres of wetlands in North America, conserving nearly 800,000 acres in California alone. Strong Valley was a proud sponsor of the recent fundraiser dinner for Fresno Ducks Unlimited. $0.83 of every $1 raised goes directly back into conservation!

Valley Animal Center, a no-kill shelter, houses thousands of dogs and cats annually until they are placed in loving homes. Their vision is to be known as the leading resource for the health and well-being of companion animals.

The majority of their shelter animals are rescued from local animal control agencies who have no more space for their animals. Even animals who have been abused, mistreated, abandoned, and injured are cared for and nurtured until a loving home is ready to adopt them. We are proud to support Valley Animal Center at their recent Golf Tournament fundraiser.

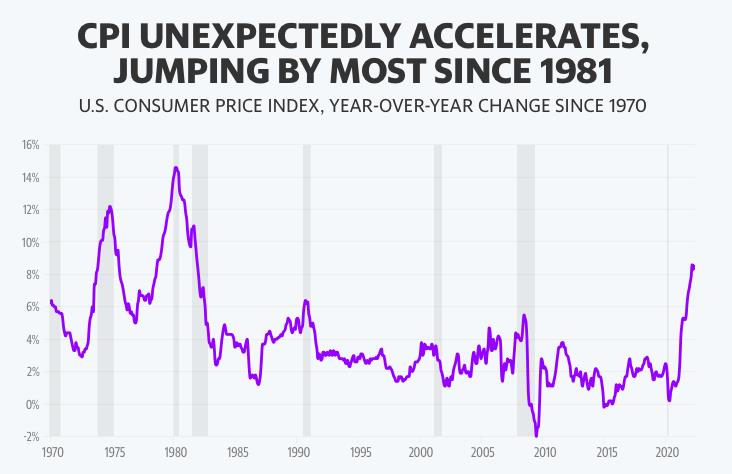

On Friday, June 10th, the U.S. Bureau of Labor Statistics reported that the Consumer Price Index for All Urban Consumers increased 1.0% in May after rising 0.3% in April. Worse, over the past 12 months, the Consumer Price Index increased 8.6%.

According to BLS, “the increase was broad-based, with the indexes for shelter, gasoline, and food being the largest contributors. After declining in April, the energy index rose 3.9% over the month with the gasoline index rising 4.1% and the other major component indexes also increasing. The food index rose 1.2% in May as the food at home index increased 1.4%.” Further:

On a 12-month basis:

Inflation in the United States has averaged around 3.3% from 1914 until 2022, but it reached an all-time high of 23.70% in June 1920 and a record low of -15.80% in June 1921.

Most will remember the high inflation rates of the 70s and early 80s when inflation hovered around 6% and occasionally reached double-digits. But so far in 2021 and 2022, inflation seems to have gone up every single month – which you no doubt already know – because you’re feeling it.

Inflation decreases the purchasing power of your money in the future and unfortunately, many don’t factor inflation into their retirement plans.

Consider this: at 3% inflation, $100 today will be worth $67.30 in 20 years – a loss of 1/3 its value.

Said another way, that same $100 will only buy you $67.30 worth of goods and services in 20 years. And in 35 years? Well your $100 will be reduced to just $34.44.

Therefore, it is imperative that your long-term retirement strategies account for inflation and

that you prepare for a decrease in the purchasing power of your dollar over time. You should strongly consider assuming that inflation will be more than 3% – its historical average.

It’s true that inflation today hovers over 8% – quadruple the Federal Reserve’s target inflation rate – but a better assumption might be one based on the last 100-years of data.

If you’re wrong and you find that the inflation rate for the next 25 years turns out to be 2%, then the purchasing power of your retirement savings will be more, not less.

Your financial advisor can create models with various inflation scenarios so you can better understand – and account for – inflation’s true impact to your retirement.

Have you ever entertained thoughts of taking an early retirement? Suppose you’re age 55 and could take home a pension income that amounted to 60% of your pay if you retire now. If your income is high, it may seem that you would be able to retire in reasonable comfort. However, before calling it quits, weigh all of the facts carefully to be sure an early retirement makes financial sense for you. Here are eight rules to consider if you’re thinking about taking an early retirement:

Retiring at age 55 with, hypothetically, 60% of your income may seem like a good deal at first. But if you wait until full retirement age, you will have another 10 years of full earnings under your belt, along with any pay increases from promotions, merit raises, and inflation. This will provide you with more money to save for retirement, and ultimately, it may boost your Social Security and pension benefits. Also, if you consider the difference in the percentage you will receive now and in 10 years¾for example, 60% if you retire now versus 80% if you retire in 10 years¾retiring now may not seem as attractive.

If you think you could manage on 60% of your income, remember that inflation will erode your pension. If you retire today and let’s say you receive a pension income of $1,600 per month for life, in 20 years at a 4% rate of inflation, you’ll have the equivalent of $707 in today’s dollars.

The longer you live, the more money you’ll need in retirement. Due to increased longevity, an early retirement plan must include a budget to meet the financial needs of several decades beyond the normal retirement age of 65.

If you already have a sizable nest egg, or if you expect to collect a pension from a previous employer, the amount of your current employer-sponsored retirement plan may not be as robust. If so, perhaps you can exit the labor force earlier because you have other sources of retirement income.

However, don’t expect Social Security to provide most of your retirement income. The Social Security Administration (SSA) projects that benefits will replace about 40% of the average worker’s preretirement income and retirees may need 70% or more of preretirement earnings to live comfortably (SSA, 2014). Also, since the future of Social Security and Medicare is uncertain, you may have to provide more funds for future health care expenses.

If you decide to leave your present job, will you be securing employment elsewhere until you permanently retire and start collecting your pension? Keep in mind that it may be difficult to find another equally high-paying position. Although the prospect of part-time work may make it possible to consider an early retirement option, be sure you can depend on a reduced part-time income until full retirement.

If you are under full retirement age andcontinue working after you begin collecting Social Security benefits, you may have to “give back” a portion of your benefits. In addition,

if you continue working after you begin collecting Social Security, a portion of your Social Security benefits might be taxed. You can determine how much of your benefits will be included in your gross taxable income with a calculator found online at the Social Security Administration’s website, www.ssa.gov.

Is there a chance your company will lay you off if you do not elect to leave on your own? Many companies now lay off high earners as part of their cost-cutting measures. If your company is experiencing financial difficulties and downsizing appears imminent, you may get a better deal through early retirement than through the company’s severance package.

If you opt for early retirement, in some cases you may incur a 10% Federal income tax penalty for early withdrawals from a qualified retirement plan. Keep in mind that withdrawals taken from an Individual Retirement Account (IRA) before age 59½ may also be subject to a penalty.

Early retirement may be a long-held dream and a financial possibility. But, before calling it quits, assess your situation carefully. You will have to live with the effects of your choice for the rest of your life. Take the time now to make sure it will be a smart decision in the long run. Your financial advisor can help.

On May 4th, the Federal Reserve raised interest rates by 50 basis points and scaled back other pandemic-era economic supports, as it stepped-up its fight against the highest inflation we’ve seen in 40 years.

“Inflation is much too high,” Federal Reserve Chair Jerome Powell said. “We understand the hardship it is causing, and we are moving expeditiously to bring it back down. We have both the tools we need and the resolve that it will take to restore price stability on behalf of American families and businesses.”

The May rate hike was the sharpest from the Fed since 2000 and the second of what is expected to be six or seven rate hikes in 2022.

In no time, the warning bells were ringing like this headline: “Lookout Retirees, Here Come Rising Interest Rates.” The headline warns us to adjust our investment strategies as bond prices, which move in the opposite direction from rates, slide.

Here is a headline from the Wall Street Journal on May 6th: “It’s the Worst Bond Market Since 1842. That’s the Good News.” But the sentence under the screaming headline said this: “The four-decade long bull market in bonds is over, but that doesn’t mean you should dump them.”

The basic premise of these warning bells and scary headlines is that Federal Reserve rate hikes will hurt bond returns so much that investors should reduce their bond allocation. Before taking cover and preparing for the impending rate raises, consider some of the faulty logic encouraging investment action.

What’s not well understood is that the Federal Reserve does not set or directly control intermediate and long-term interest rates that matter most to bond prices. The federal funds rate affects extremely short-term rates, and thus has a strong impact on the yield of money markets, bank savings accounts and floating rate loans. It has much less influence on longer-term rates, which are a function of bond investors’ trades and market expectations.

Let’s go back to a period of Federal Reserve rate hikes which began in June 2004 for a clear example of the disconnect between the fed funds rate and longer-term interest rates. On June 29, 2004, the day before the Federal Reserve began to increase rates, the 10-year U.S. Treasury yielded 4.7%. Within three months of the first rate hike, the 10-year’s yield declined below 4.0%.

That is, the Fed increased rates, but bond yields went the opposite direction. A year after the first rate increase, the 10-year Treasury yield remained below 4% despite the fed funds rate increasing by two percentage points over that span.

Purchasing a 10-year Treasury the day before the Fed started raising rates and holding it for a year resulted in a return of 10.1%. A 20-year Treasury held over that same time earned 19.2%.

One reason: Back then, China’s government was an eager buyers of long-term Treasuries, which drove up their prices and pushed down their yields. Today, that might not be the case, but for many foreign investors, especially amid troubles in Eastern Europe, long Treasuries are the safe-harbor investment of choice. So much for the concept that you don’t want to own bonds when the Fed is increasing rates.

If the market anticipates that Fed rate hikes are likely to trigger an economic slowdown, recession or simply curtail any inflation pressures, expect longer-term bond yields to decrease, not increase.

It’s a fallacy to simply say that higher interest rates will hurt bond returns. This belief holds true in the short-term, but not in the longer-term. If you buy a 10-year Treasury today and you’re seeking the highest nominal return over the next decade, the best-case scenario is that interest rates rise dramatically immediately after you purchase the bond.

This logic flies in the face of traditional short-term thinking because most people associate rising interest rates with lower bond prices. True, the bond price will decline in the short-run and you would have been better waiting to buy the bond after rates increased, not before.

But if rates immediately rise, you will be able to reinvest the coupon payments at higher reinvestment rates over the next 10 years, which will make for a higher holding period return over the bond’s decade-long term than if rates had remained constant or declined.

It’s also a fallacy to think that you should sell bonds in advance of Fed rate hikes. Again, remember that bond yields are not directly tied to the federal funds rate. Plus, anyone who sells bonds has to find a replacement investment for the sale proceeds.

Cash still pays nearly nothing and stock prices have historically provided lackluster results in rate tightening cycles. Also, predicting outcomes is a fool’s errand. Timing the movement of interest rates has dumbfounded investors for decades and is likely to continue doing so.

If you think you clearly know the future path of interest rates, you are better served to open a hedge fund and make outlandish profits, than to simply make a few dollars on your own portfolio. Bonds in a diversified portfolio provide protection in stock market selloffs.

While the Standard & Poor’s 500 lost 36.6% in 2008, an investment in 10-Year Treasuries gained 20.1%. If you’re worried more about sharp portfolio losses than near-term fluctuations, a better idea is to maintain a bond allocation, rather than to abandon this protection.

What do these fallacies of rising interest rates mean to you? Humans are inherently biased to do something, a point that is not lost on Wall Street. People prefer action over inaction, regardless of whether inaction is optimal. Since Wall Street profits from investor activity, there will continue to be warnings of rising interest rates and what you can do to protect yourself. as banks and brokerages have a vested interest in compelling trading activity.

Don’t let public perceptions drive your bond investing. Remember the difference between speculation and investment.

In the words of author Fred Schwed Jr., a stock trader who got out of the market in 1929:

“Speculating is an effort, probably unsuccessful, to turn a little money into a lot. Investment is an effort which should be successful, to prevent a lot of money from becoming a little.”