Call Our Office

(559) 384-2900 | Fresno

(619) 480-1413 | San Diego

(619) 480-1413 | San Diego

Your Money

Your Life

Your Way

You are now leaving the Strong Valley Wealth & Pension, LLC ("Strong Valley") website. By clicking on the "Schwab Alliance Access" link below you will be entering the Charles Schwab & Co., Inc. (“Schwab”) Website. Schwab is a registered broker-dealer, and is not affiliated with Strong Valley or any advisor(s) whose name(s) appears on this Website. Strong Valley is/are independently owned and operated. Schwab neither endorses nor recommends Strong Valley. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Strong Valley under which Schwab provides Strong Valley with services related to your account. Schwab does not review the Strong Valley website(s), and makes no representation regarding the content of the Website(s). The information contained in the Strong Valley website should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.

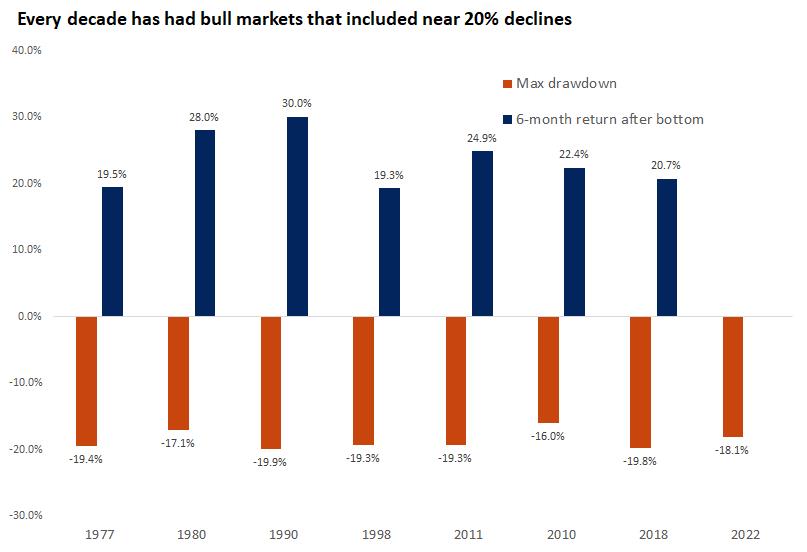

The standard definition of a bear market is when major U.S. stock indices, such as the S&P 500, drop by 20% or more from their peak. And 5+ months into 2022, we see NASDAQ and the smaller-cap Russell 2000 both in the grips of a bear and the DJIA and S&P 500 darting just outside the claws of a bear (by the time you read this, they could both very well be trapped by a bear or be further away from the claws).

Let’s examine the last time the S&P 500 was in a bear market and a little history of other past bear markets.

Remember when the S&P 500 closed at a then record high of 3,386 on February 19, 2020 and just three short and very painful weeks later, the S&P closed under 2,500, a drop of 26% in about 16 sessions (the COVID-bear)?

Then, on August 17th, the S&P 500 eclipsed that February 19th high in mid-morning trading, and it mostly managed to stay above that level. In fact, it was the second fastest-ever bear market to market peak in history as it took 126 trading days for the S&P 500 to reclaim its February high.

And this was over 10 times as fast as the index’s average historical rebound (1,542 trading days).

One the one hand, it was the fastest bull-to-bear market in history (COVID). But on the other hand, it was the second fastest bear market recovery in history.

From the perspective of an investor, there really is nothing special about that 20% threshold that separates a correction from a bear market. Does it matter if the S&P 500 is down 19% versus 21%? Both scenarios probably leave you feeling anxious. But it is worth remembering that every decade has seen bear markets and bull markets.

Glass half-full investors will undoubtedly focus on the good news – the worst decline in our economy since the Great Depression (the COVID bear) took just 126 days to recover – maybe we will see a similar recovery.

And glass-half-empty investors will undoubtedly focus on the not-so-good news – inflation is at 40-year highs, we have 11 million open jobs, the Fed is raising rates aggressively and corporate earnings are coming in weak – this bear will be more like other historical bears.

But long-term investors would be well served understanding both perspectives.

Consider this simple bittersweet example:

Be honest, how does this make you feel? Probably happy on the one hand, less so on the other, right?

What should you do? Well, the answer to that question, of course, is deeply personal. That being said, it’s never a bad idea to better understand the current macro-economic environment to help make informed decisions.

But the important point to keep in mind is that all the macro-economic data in the world is only helpful as it informs your long-term investing decisions and asset allocations. So before you make any investing changes, make sure you talk to your financial advisor to ensure that your assumptions are consistent with your risk profile and your financial plan.

Every day in Fresno and Madera counties, at community centers, high schools, middle schools, juvenile institutions, coffee shops, and local hangouts, Youth for Christ staff and volunteers meet with young people.

Fresno/Madera YFC is a rural, suburban, and urban non-profit ministry on a mission to share the saving love of Jesus with teens, especially those living in group homes. Their focus is to bring young people closer to God and closer to each other. We were pleased to be a participant sponsor at the recent Golf Classic fundraiser for YFC on May 5th. They are making a positive difference in our communities and in our youth.

Too often during uncertain times, we inadvertently compare ourselves to the people around us – and that leads us to make financial mistakes.

In his book Predictably Irrational: The Hidden Forces That Shape Our Decisions, Dan Ariely remarks, “We don’t have an internal value meter that tells us how much things are worth. Rather, we focus on the relative advantage of one thing over another, and estimate value accordingly.” Later he adds, “We not only tend to compare things with one another but also tend to focus on comparing things that are easily comparable.”

In other words, we use completely irrelevant benchmarks to gauge our success and make decisions. We compare the car we drive or clothes we wear to our siblings. We draw comparisons about how our children act relative to the neighbors.

None of these comparisons makes rational sense. Instead they take the common shortcut and follow things easily comparable to a simple, concrete – and irrelevant – answer.

Simple comparisons also often gloss over details. In another example, you lament that you refinanced your mortgage at 4% interest while your brother got 3.75%. The interest rate provides a simple comparison and misses the big picture.

Digging deeper, we find that your brother paid closing costs and you didn’t. The monthly savings of that 0.25% difference covers the closing costs after 10 years but your brother only wants to stay in the home for five. The lower rate ends up costing more.

Nowhere is relative benchmarking more prevalent and more irrelevant than in investing. How you perform against the Standard & Poor’s 500 bears little on your financial well-being.

If you are in retirement and have a properly structured portfolio, you probably underperformed the S&P 500 since the onset of COVID and maybe have outperformed YTD so far in 2022. Big deal. The S&P 500 is not trying to accomplish with its money what you try to accomplish with yours.

For instance, if you ever owned a business, you understood that revenue and profits rise and fall. It is not always a consistent upward trajectory. You continue running your business because of the lifestyle it provides, and you make decisions that ensure continuity. Few owners run their business to maximize returns at all times – those that do are often hung out to dry when things get rough.

Consider your retirement portfolio as your own small business, comprising ownership in thousands of real, functioning businesses.

If you strive to maximize gains in all the businesses at all times, you eventually get burned. Not to mention that the business (portfolio) performance of the bicycle shop guy down the street bears no relation to that of your bakery.

That comparison makes no sense. Your portfolio provides you with the lifestyle you want.

Blindly comparing your portfolio to an arbitrary benchmark – especially over short periods – tells you nothing about whether your investments help you toward your life goals. There’s nothing less relevant.

Actors Johnny Depp and Amber Heard are in a contentious defamation trial in a Virginia court. Depp and Heard were married from 2015-2017 (15 months) and Depp is suing Heard for $50 million over a 2018 op-ed she wrote for The Washington Post in which she described herself as a "public figure representing domestic abuse." Though Heard did not specifically name Depp in the article, he claims it cost him lucrative acting roles.

But it was another pair of lawsuits involving Johnny Depp's assets that might be more relevant to those questioning the importance of estate planning. Because with about 40 million lawsuits filed in the U.S. each year, protecting your family's legacy and assets is getting harder and harder.

In 1999, Depp hired The Management Group to handle his expenses as his business manager. By then Depp had become a very wealthy actor who led a lifestyle that included 14 homes, a $75 million yacht and $30,000 a month for wine.

And as hard as it might be to believe, Depp's lifestyle cost him in excess of $2 million per month, which according to his business manager, was far exceeding his cash flow.

In January 2017, Depp hired a new business manager and conducted a financial analysis of his assets. During this analysis, he claimed to have discovered big investment losses made by The Management Group, so he filed a lawsuit seeking damages of $25 million.

The Management Group responded with a countersuit of their own alleging that early in Depp’s career, he borrowed $5 million from them to cover the expenses of his lifestyle and had allegedly defaulted on this loan. The countersuit sought to recover his loan by foreclosing on some of Depp's assets.

The lawsuits were eventually settled.

There are a lot of lessons to be learned from Depp's experiences – and it's not that the rich are different.

If Depp had established an asset-protection plan, he could have ensured that his personal wealth was protected from any potential lawsuits. In effect, it would have placed his assets under the ownership of a trust.

Depp would not legally own the assets, as they would be owned by the trust itself – protected from any lawsuits brought against him.

There's a lesson in that Johnny Depp saga: Protecting your assets and family's legacy should always be an important part of any comprehensive estate plan.

As such, you should consider placing your assets into a protective trust. And there are a few to choose from.

There are a lot of considerations when selecting the right trust for your situation. For example, you want to make certain that the trustee has hired a reputable investment manager for your assets. In addition, you want to make sure the professionals and fiduciaries have the requisite checks and balances in place.

Your financial advisor can help you select the right trust for your circumstances. It’s part of your personal estate planning process.

“Not All Treasure is Silver and Gold Mate.” ~ Captain Jack Sparrow

When Jill and John Smith purchased their life insurance policies ten years ago, they based their coverage on their anticipated obligations and needs. They made policy decisions, taking into account the mortgage on their home, projected college education costs, and living expenses. Well, that was then – and this is now.

Recently, the Smiths reevaluated their insurance needs and were surprised to discover their insurance coverage was inadequate. How could this be? The answer is really quite simple – inflation.

Because inflation affects future purchasing power, it also affects future life insurance needs. For couples like the Smiths, inflation means that life insurance coverage, which may have been adequate several years ago, may no longer be sufficient. With this in mind, consider three of the more common life insurance needs that may be affected by inflation.

Until recently, it seemed that many people who bought their homes lived in them for most of their lives. Today, Americans are increasingly mobile. Changing employment opportunities, the work-from-home movement, along with dual incomes, have altered the dynamics of family finances.

In many cases, a growing family may now be able to afford to pay a mortgage on a lot more “house” than at any time in the past. Does this trend minimize the reality of inflation and the rising costs of homeownership? Not at all.

The fact is, escalating real estate prices have translated into larger mortgage loans. Therefore, if you have recently purchased a home, you may need to consider increasing your life insurance to help cover your new mortgage.

If you are planning on sending your children to college, you are probably concerned about the escalating costs of higher education. And, rightfully so.

The average cost of college in the United States is $35,720 per student per year. The cost has tripled in 20 years, with an annual growth rate of 6.8%. The average in-state student attending a public 4-year institution spends $25,615 for one academic year.

To be prepared, factor inflation into your college savings strategies. Make sure you have adequate life insurance to help provide financial protection in the event of an untimely death, and consider increasing your coverage so that it best reflects the future cost of education.

Shopping at the grocery store. . .pizza on Friday nights. . .taking your children to the movies. . .filling up your gas tank. . .purchasing a new car. Over the course of time, the costs associated with these necessities and “treats” of everyday life are affected by inflation.

As a result, your family’s future lifestyle could be affected too. By basing your life insurance needs on your current income and today’s cost of goods and services, you are potentially shortchanging your family’s future. Be sure to account for increases in the cost of living as you insure your family’s current and future financial security.

Determining your current life insurance needs is one thing. But, figuring out how much coverage you’ll need in the future requires you to pay careful attention to inflation and how it can affect your lifestyle.

Regular reviews of your insurance coverage can help you keep pace with inflation and your changing needs. Make the necessary updates before you need them.

Strong Valley was pleased to support the recent Gala of Wishes in Fresno. Hosted by the Central California chapter of the Make-A-Wish Foundation, this annual gala raises money to grant wishes for children battling critical illnesses. Since the chapter was founded in 1983, it has granted more than 9,000 wishes for children across Central California. The event kicked off at The Painted Table with a cocktail reception and raffle, followed by a dinner prepared by Chef de Cuisine.

Some of us may remember the “good old days,” when gasoline prices were as low as 25¢ per gallon. Others may recall when a can of soda cost 15¢. But prices tend to rise over time – sometimes steadily and sometimes abruptly. In the years ahead, inflation will most likely decrease the purchasing power of your money, which means that during retirement, your dollars will buy less than they do today.

It is easy to misinterpret inflation as the rise in price of individual goods and services. However, inflation is the increase in the averageprice level of all goods and services.

For example, the price you pay for oranges may rise during the winter due to unseasonably cold temperatures in Florida. On the other hand, the average price of other items in your local supermarket, like peanut butter and paper towels, may remain relatively level. So, the increase in the price of oranges is not a result of inflation but, rather, a function of supply and demand.

Inflation can result when either:

Note how, as inflation is defined here, the supply and demand for oranges alone would have no effect on inflation. However, changes in supply and demand on a broader scale can result in inflation.

Consider the following economic scenario: suppose business is booming, unemployment is low, and the average worker’s wages are increasing. As a result, consumers have more disposable income available and may therefore be able to purchase more goods and services. Average prices tend to rise under these circumstances due to the increase in demand for all goods and services.

In another scenario, suppose the economy is suffering. As unemployment rises and wages remain stagnant, consumers may be unable to purchase additional goods and services. Production may then slow down, with prices going up to minimize the losses. In this cycle, average prices tend to rise due to a decrease in the supply of all goods and services.

It is important to keep in mind that individual consumers are not the only participants in the market that can affect the economy. Businesses, government agencies, and foreign markets also spend billions of dollars on U.S. goods and services. Their spending, or lack thereof, can equally influence increases or decreases in supply and demand that, in turn, can result in inflation.

To a certain extent, some inflation may be a sign of a healthy economy. In fact, one of the economic policy goals of the U.S. government is to maintain an inflation rate ranging from 0% to 3% per year (2% is the stated goal). Too much inflation or no inflation at all can be a sign of troubling economic times. So one of the greatest challenges facing policymakers is making decisions that lead to the optimum level of inflation.

Two Federal economic policies are used in an attempt to control the economy. Fiscal policy, which falls under the auspices of Congress, uses taxation and spending to reach full employment, stabilize prices, and boost economic growth. In contrast, monetary policy, which is controlled by the Federal Reserve Bank (the Fed), manipulates the money supply and short-term interest rates in an attempt to spur growth or control inflation.

Congress, and especially the Fed, looks at the Consumer Price Index (CPI) when making policy decisions. The CPI is considered by many to be one of the best measurements of inflation. The CPI gauges the average change in prices paid by urban consumers for a fixed market basket of goods and services over a period of time. The CPI represents all goods and services purchased by urban consumers. Each month, the CPI is calculated, and constant fluctuations in the CPI will ultimately result in Congress or the Fed taking appropriate measures to regain control of inflation. Note that the Fed has the ability to react quickly. However, Congress must pass legislation, which requires debate and time, before its fiscal decisions can be carried out.

In addition to creating higher costs for goods and services, inflation creates depreciation in currency values. So, as prices increase, the purchasing power of your income – dollar for dollar – decreases. During sound economic times, price increases will usually be accompanied by wage increases that are equal to, or greater than, inflation. However, during economic downturns, when wages remain level, the cost of living increases as your purchasing power diminishes.

Regardless of what state the economy is in, one of your greatest long-term financial challenges may be planning for your retirement savings to outpace inflation.

Therefore, it is always important to consider inflation, not only as you save, but also as you make purchasing decisions.

Your financial advisor can help you plan.

The Internal Revenue Service announced that the amount individuals can contribute to their 401(k) plans in 2022 has increased to $20,500, up from $19,500 for 2021 and 2020.

From the IRS website:

“The contribution limit for employees who participate in 401(k), 403(b), most 457 plans, and the federal government's Thrift Savings Plan is increased to $20,500, up from $19,500.

The income ranges for determining eligibility to make deductible contributions to traditional Individual Retirement Arrangements (IRAs), to contribute to Roth IRAs, and to claim the Saver's Credit all increased for 2022.

Taxpayers can deduct contributions to a traditional IRA if they meet certain conditions. If during the year either the taxpayer or the taxpayer's spouse was covered by a retirement plan at work, the deduction may be reduced, or phased out, until it is eliminated, depending on filing status and income. (If neither the taxpayer nor the spouse is covered by a retirement plan at work, the phase-outs of the deduction do not apply.)

Here are the phase-out ranges for 2022:

The income phase-out range for taxpayers making contributions to a Roth IRA is increased to $129,000 to $144,000 for singles and heads of household, up from $125,000 to $140,000.

For married couples filing jointly, the income phase-out range is increased to $204,000 to $214,000, up from $198,000 to $208,000. The phase-out range for a married individual filing a separate return who makes contributions to a Roth IRA is not subject to an annual cost-of-living adjustment and remains $0 to $10,000.

The income limit for the Saver's Credit (also known as the Retirement Savings Contributions Credit) for low- and moderate-income workers is $68,000 for married couples filing jointly, up from $66,000; $51,000 for heads of household, up from $49,500; and $34,000 for singles and married individuals filing separately, up from $33,000.

The amount individuals can contribute to their SIMPLE retirement accounts is increased to $14,000, up from $13,500.

The limit on annual contributions to an IRA remains unchanged at $6,000. The IRA catch-up contribution limit for individuals aged 50 and over is not subject to an annual cost-of-living adjustment and remains $1,000.

The catch-up contribution limit for employees aged 50 and over who participate in 401(k), 403(b), most 457 plans, and the federal government's Thrift Savings Plan remains unchanged at $6,500. Therefore, participants in 401(k), 403(b), most 457 plans, and the federal government's Thrift Savings Plan who are 50 and older can contribute up to $27,000, starting in 2022. The catch-up contribution limit for employees aged 50 and over who participate in SIMPLE plans remains unchanged at $3,000.”

As you can see, there are a lot of rules, deadlines and contribution limits that change from year to year. Further, many of these might be helpful to your situation – but many might be inappropriate too.

Talk to your financial advisor as you consider your 2022 financial plans.

Source: irs.gov