Call Our Office

(559) 384-2900 | Fresno

(619) 480-1413 | San Diego

(619) 480-1413 | San Diego

Your Money

Your Life

Your Way

You are now leaving the Strong Valley Wealth & Pension, LLC ("Strong Valley") website. By clicking on the "Schwab Alliance Access" link below you will be entering the Charles Schwab & Co., Inc. (“Schwab”) Website. Schwab is a registered broker-dealer, and is not affiliated with Strong Valley or any advisor(s) whose name(s) appears on this Website. Strong Valley is/are independently owned and operated. Schwab neither endorses nor recommends Strong Valley. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Strong Valley under which Schwab provides Strong Valley with services related to your account. Schwab does not review the Strong Valley website(s), and makes no representation regarding the content of the Website(s). The information contained in the Strong Valley website should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.

The January Effect is a pattern exhibited by stocks in the last few trading days of December and the first few weeks of January. During this period, particularly starting in January, the theory is that stocks tend to rise.

In simple terms, the January Effect is a consequence of:

Because so many of these stocks were sold in late December, they will be – in theory – available at a discount in early January. Another purported cause of the January Effect is the payment of year-end employee bonuses (less likely in 2020), which employees invest in the stock market. As a result, investors with more money end up buying cheaper stocks, making the market more active and driving up prices.

The January Effect is notjust a Wall Street myth as several prominent studies have confirmed its existence. One study of historical data from 1904 through 1974 discovered that the average return during January was five times larger than the average return for other months.

Another study by the investment firm Salomon Smith Barney (no longer in existence by the way) showed that small cap stocks (as represented by companies in the Russell 2000) outperformed large cap stocks (as represented by companies in the Russell 1000) by 0.8% in January, but lagged large caps for the rest of the year.

Further, consider this:

In recent years, the January Effect has become less pronounced. As a result, it is a less effective way for investors to take advantage of the market. Once investors, economists and traders spot, analyze, and confirm the existence of a trend, it tends to become less pronounced.

Investors “price in” the trend, adjusting their investment strategies to take trends (like the January Effect) into account. Another reason that the January Effect is less important is that many people now use tax-sheltered retirement plans, like IRAs and 401(k) plans. When investments are tax-sheltered, there is no special reason to sell a stock for the purpose of deducting stock losses.

Many investors and analysts have tried to use the January Effect for predictive value. However, there are different questions about predictions.

Surprisingly, according to Stock Trader’s Almanac, going back to 1950, that metric ofJanuary’s monthly performance predicting the year has worked about 87% of the time.

But if you take out the years from 1950-1962, the January metric worked about as well as a monkey making a coin toss. From 1962 to 2020, a below-par January accurately predicts a bad year 55% of the time.

As these numbers show, the January Effect is simply not a very good predictor of annual stock market performance. Of course, the S&P 500 has risen about 8.19% on average (including dividends) from 2000 through 2020.

As a result, omens in January are unlikely to predict the entire year.

It’s easy to lose or misplace money. But unlike finding $20 in an old jacket, what if a bank or investment account containing thousands goes untouched for years because you forgot about it or never told anyone it existed?

For various financial accounts, holdings, investments, loans, tax returns, and other arrangements, you need to gather account information and relevant contacts. If you’re wondering why it’s worth taking the time to get all this info in one place, just think of the people you love. By organizing your financial and legal documents, if something happens to you your family can more easily:

First, you need to determine all the types of accounts you have. Here’s a comprehensive list to get you started:

After you’ve identified all the accounts you have, here’s the information you need to gather for each. Tip: The details for each account or asset may vary, so just pointing a person you trust in the right direction -- like giving them the name of your financial advisor -- will be super helpful.

Type of Credit Card: Visa | MasterCard | American Express | Discover | Diner’s Club | JCB | Store/Gas Card | Other

How do you prepare your taxes? (You could answer this question out loud but that won't really do anything. Except maybe scare the cat. So keep track of it.)

Share the name and contact info of this professional.

What software/service do you use? How do you login to this account?

No Matter What: Tell someone you trust where you keep your past tax returns! If something happens to you, these are an ideal financial blueprint for people in your life to understand your estate.

Keeping important documents (deed to your house, insurance policies) and valuable items (heirlooms, jewelry) extra safe is smart. Not giving someone access in case something happens to you can turn into a long detour through the courts.

This is especially troubling if you kept your Will or other important documents your family might need in a safe deposit box. Solution: Check with the bank where you’re renting a box and name a designee or whatever they might refer to this person as.

Now, onto the details to share:

Don’t let any loans your family and loved ones are unaware of sneak up on them. Keep track of the following info and once the loan is paid off feel free to mark it “PAID” and celebrate.

Type of Loan: Line of Credit | Personal Loan | Student Loan | Other

Make sure all of the stuff listed above is neatly organized, updated, and shared.

Cleaning up personal finances remains one of the top resolutions every New Year. But we all know what happens to most such self-promises, so here’s a month-by-month to-do list to cultivate better financial health.

January: Organize paperwork. This obvious starting point eludes many. Are your financial documents organized, in paper or virtually, so information is at your fingertips? Your heirs will be eternally thankful if you unexpectedly die or are incapacitated.

February: Consolidate investments. Trim your number of accounts and consolidate all your dormant 401(k)s into individual retirement accounts. Spreading your assets across various brokerage accounts is not smart diversification – it’s a recipe for confusion.

March: Follow the money. If you’re still working and too busy with your life, you may have a poor sense of your personal cash flow, the money that comes in and where you spend it. You can’t establish how much you save or spend without knowing where you are right now.

April: Tax smarts. It’s better to owe your state and the federal government instead of overpaying throughout the year.

Did you fund an IRA for your spouse, max out funding on your defined contribution plan at work or fund your Roth IRA by the April 15th deadline? Did you track your losses on your taxable accounts, such as individual and joint investment accounts, bank accounts and money market mutual funds, to name a few? These moves can qualify you for tax credits.

May: Investment smarts. How much do your investments cost you? Do you know what your insurance agent, 401(k) plan or financial advisor charges? How about the underlying expenses you pay to buy mutual funds or exchange-traded funds?

Are your investments allocated wisely to minimize taxes? For example, do you hold real estate investment trusts in your tax-deferred account? Municipal bonds in your taxable account? How much risk do you take?

June: What are you worth and why it matters. You can calculate your net worth (all your assets, such as your home and retirement funds, minus all your liabilities, such as your mortgage and credit card debt) many ways. A sophisticated net-worth calculation projects factors of asset growth such as rates of investments’ returns and risk and your rate of saving and liabilities to the end of your life.

Your goal: Minimize the risk of outliving your assets.

July: Insure against risk. Insurance keeps you financially whole if disaster strikes. To cite two examples of policies to review, did you outlive your 20-year term life insurance? If so, you’re a winner because you remain alive yet you need to consider more coverage.

Have you considered long-term care insurance, especially if you’re a woman with a longer life expectancy than a man? This coverage helps with costs of basic daily needs over an extended time.

August: Retirement planning. This planning starts in your 20s and does not end when you retire. If you’re employed, know when you can afford to retire (assuming you’re not laid off).

Are you aware of all strategies to maximize Social Security payouts? If retired, are you withdrawing from your accounts in the correct order? (Start with your taxable holdings, then move on to tax-deferred and then untaxed.) Calculating optimal distributions from IRAs and other taxable income sources annually can trim your taxes.

September: Preparing for the inevitable. Engage an estate attorney. If you die without a will, your state of residency distributes your assets with no input from you.

If your estate documents are older than about seven years, refresh them. Everyone needs such estate documents as wills, living wills, medical health-care directives and powers of attorney to stipulate your wishes if you become unable to decide matters yourself.

You especially need these papers if you or your spouse, or both, are uncomfortable with financial matters and your children are younger than legal age.

Also, draw up or re-examine these documents if:

October: Gift wisely. You can give back in many ways to organizations and people you care about with donations of appreciated securities or with payments on college loans or new mortgages. The Internal Revenue Service offers several guidelines on gifting.

Your greatest gift may be taking care of yourself so you don’t eventually become a financial burden to your adult children.

November and December: Reality check. If you followed these steps, you’re in the minority of individuals with the tenacity to tackle financial planning.

But you still should engage a professional advisor to check your assumptions. Be realistic about what you can accomplish on your own.

It’s important to get your finances right and keep them right all year.

Sometimes, when most people believe the same thing, a big change is on the way. That thinking is known as contrarian. The housing market may be primed to give us a big lesson in contrarianism. If so, that’s not-so-good news for homeowners and real estate investors.

Contrarian theories abound concerning the herd mentality of investors. You could argue it was as much of a death note for the market as for an athlete featured on the cover of Sports Illustrated.

We are not too terribly worried when we see only one article of this nature. But when the topic appears in many news articles, it is a potential red flag, although not a guarantee that anything will happen. The psychology of the cover curse is that, by the time something is the conventional wisdom and graces magazine covers, it has peaked.

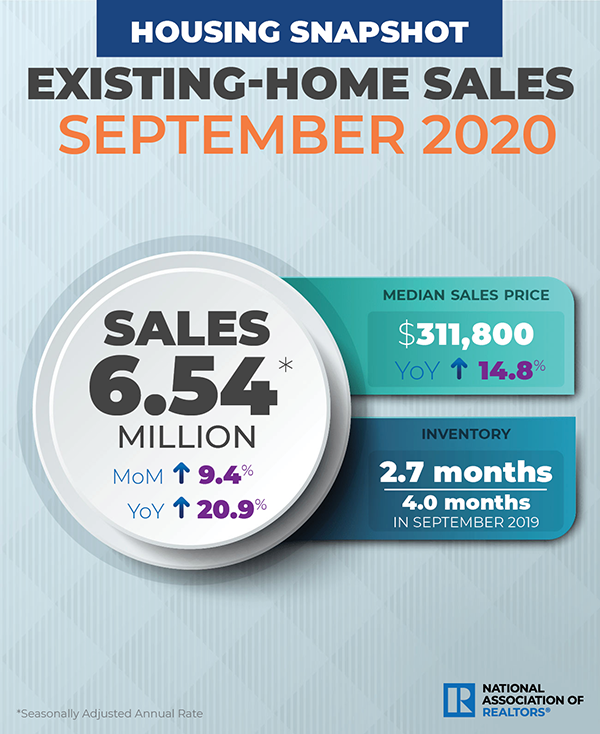

The same contrarian thinking could be applied to the housing market, which by all accounts is sizzling in 2020.

According to the National Association of Realtors, existing-home sales grew for the fourth consecutive month in September as each major region saw month-over-month and year-over-year gains, with the Northeast seeing the biggest jumps.

Here are a few highlights:

The highlights above paint a robust picture of today’s housing market and whether we’re headed for – or are already in the midst of – a bubble is really anyone’s guess. Unfortunately, we usually don’t see a bubble until it has already popped.

But consider some of the other statistics from the NAR:

Remember the “Location, Location, Location” mantra preached by realtors everywhere? Well, look at what the four major regions in the U.S. have experienced:

While home prices continue to soar, interest rates are at historical lows and inventory is tight, remember when someone says: “this time it’s different.”

Because nothing goes up forever.

After his grandfather died more than a decade ago, Lamarr Couser and his family were caught by surprise when the funeral director asked whether the World War II veteran was covered by a life insurance policy from the Department of Veterans Affairs.

Couser, who is himself a U.S. Navy veteran and former National Guardsman, wasn't aware of the VA life insurance, a $10,000 policy for disabled veterans who might otherwise be denied private coverage, nor had he yet applied for it. His grandfather didn't have it, either. "I was shocked," he says. "It must be one of the best-kept secrets there is."

Indeed. The insurance is just one of several substantial benefits for many veterans and their families--from insurance to caregiving--that you may never have heard of. Consider Aid and Attendance, a tax-free benefit that helps cover an eligible veteran's costs for caregivers, nursing homes or assisted living--in some cases, to the tune of nearly $2,000 a month.

Many vets may also be unaware that the VA recently made it easier for veterans to get hearing aids, says Louis Celli, director of Veterans Affairs and Rehabilitation for the American Legion. No longer does a vet need a physician's referral to get an appointment with a hearing specialist. He or she can simply schedule an appointment. VA insurance covers the cost; Medicare typically doesn't.

And in March, the VA said it will recognize eight diseases linked to contaminated water at Camp Lejeune, N.C., and cover claims for veterans suffering from those ailments who served there at least 30 days between August 1, 1953, and December 31, 1987.

"There's a whole framework of resources out there," says Joseph Montanaro, a financial planner with USAA's military affairs advocacy group. Don't assume you're not eligible, he says. And recognize that spouses and dependents may qualify, too.

Montanaro's family learned that lesson when his father died of a service-related lung disease. They were surprised to discover their stepmother qualified for Dependency and Indemnity Compensation, a monthly tax-free payment for surviving spouses and dependents that can total more than $1,200, Montanaro says.

It's not just career military vets who can qualify for benefits. In general, veterans who served before 1980 need only have 90 days or more of active duty and a discharge other than dishonorable to qualify for many benefits. Veterans who served after 1980 must have served 24 continuous months of active duty or the full period for which they were called to active duty.

Ignore the common myth that you have to be disabled to use VA health care. You can check your eligibility at www.vets.gov/healthcare/eligibity. Co-pays may be required, depending on income and other factors.

Seek help from veterans' groups such as the American Legion, the Veterans of Foreign Wars (VFW), the Disabled American Veterans (DAV) and the Vietnam Veterans of America (VVA). Through those organizations' websites, you can find a veteran service officer in your area who can point you toward benefits you might be eligible for, help you apply and assist in appeals. Their services are free.

As a first step, be sure to fill out an intent to file form covering the specific benefit you seek, says Kaylin Gilkey, community engagement manager for Veteran-Aid.org, an advocacy group. It may take months for your claim to be approved, but your benefits will be retroactive to the date you filed the form. That could mean thousands of dollars in reimbursements, she says. If a veteran dies while a claim is outstanding, it can be pursued by a surviving spouse or dependents, says Michael Figlioli, deputy director of the VFW National Veterans Service.

Spouses and dependents of a permanently and totally disabled vet can qualify for health insurance through the VA's Civilian Health and Medical Program, or CHAMPVA. "It can be a huge savings, for you and your family," says Chad Moos, the DAV's deputy national service director. "But some veterans have gone years and years without even realizing their dependents are eligible." There are no premiums for CHAMPVA health and prescription coverage. Those on CHAMPVA can also sign up for Medicare Part D, which does have premium costs; Medicare is always the primary payer.

For veterans who need more help at home, there's a "hidden benefit" known as the Veteran-Directed Care Program, says Adrian Atizado, DAV's deputy national legislative director. It allows certain disabled veterans to hire family and friends to help with daily living tasks, such as doing the laundry or helping with breakfast. The VA provides you or your financial counselor as much as $2,000 a month, on average, to pay caregivers and aides you choose. The program is available through VA Medical Centers in at least 35 states.

Vietnam War vets who may have been exposed to Agent Orange, a herbicide used during the war, are eligible for a range of compensation and health care benefits. To qualify, you need to prove that you had "boots on the ground" in Vietnam, even briefly, between January 9, 1962, and May 7, 1975. You also need to show that you have a current diagnosis of one of the disabilities recognized by the VA as linked to the exposure, such as diabetes mellitus Type 2 or ischemic heart disease. Vets exposed to Agent Orange aboard ships, on aircraft and in other locations can also qualify.

If you meet the requirements for Agent Orange-related benefits, you may obtain disability compensation benefits and access to other health services more quickly, says Kelsey Yoon, director of veterans benefits for the VVA. And children of veterans exposed to Agent Orange who were born with spina bifida and certain other birth defects may also qualify for benefits, including compensation, health care and vocational training. "Older vets especially worry about who is going to take care of their kids when they're gone," Yoon says. "This is one of the most unknown benefits."

For long-term care, the Aid and Attendance benefit is aimed at helping older veterans and their spouses when they can no longer handle daily living tasks, such as dressing and showering, on their own, says Veteran-Aid's Gilkey. To qualify, you usually need to be paying for some kind of care, have roughly $80,000 or less in assets (excluding one home and one vehicle) and have served at least one day during wartime while on active duty. The $80,000 figure is a rough estimate, Veteran-Aid notes, and you can sometimes qualify above that limit. A single veteran can receive as much as $1,794 a month; a surviving spouse, $1,153; and two married veterans as much as $2,846. "It's been around a long time, but it's still so little-known," Gilkey says.

Vets who have mobility problems can apply for grants available to modify a car or home. There are also state VA benefits, from exemptions for local property taxes to free fishing and hunting licenses. For details, see the State Veteran's Benefits map at Military.com, a benefits information site.

After a veteran's death, survivors may qualify for benefits such as the monthly benefit payment that Montanaro's stepmother received. You could be eligible if the veteran died in the line of duty or from a service-related cause, says Kevin Friel, assistant director of the VA's pension and fiduciary service.

The VA can help with some burial expenses, and it provides a free headstone or marker and burial flag. The VA just created a program that allows veterans to apply for burial benefits in advance, so veterans and their families can plan ahead. Go to www.cem.va.gov/pre-need to learn more.

Open enrollment for employee benefits kicks off on November 1st. Before you plan your Thanksgiving menu, you should make the time to review your benefit choices.

Employee benefit experts expect benefits to change next year like few years before – given the rising costs of health care and the impact of COVID-19 on businesses this year. Even if little changed in your life in 2020 – and that’s probably unlikely – you should aim to maximize what your employer offers.

Here are a few pointers.

Even if you carry the same plan as in many past years, spend a few minutes evaluating which one is best for you and your family when you choose – especially High-Deductible Health Plans and traditional plans.

Switching from the traditional plan to a high-deductible option might save money if you don’t visit the doctor much. Perhaps too your spouse’s company now offers a better plan and you can switch the family coverage to the better alternative.

Improved employer plan descriptions lay out plans’ differences and costs and do that much better this year. Take advantage of their free help, online or in person.

Often you receive only one choice for dental coverage, but you might be surprised at how many people decline to pay the relatively small premium for this coverage. Even if young and cavity-free, you take care of your teeth now to potentially prevent large dental bills in retirement.

If nothing else, dental insurance provides a teeth-cleaning twice a year.

This benefit works great if you wear glasses or contacts and need regular eye exams. Those with perfect vision may opt out of this coverage.

Most employers offer some basic life insurance, the coverage usually a multiple of your salary. If you are married, own a home or have kids, this basic coverage usually falls short.

Consider paying extra if possible, to increase life coverage through your employer. If that’s not an option, consider supplementing this minimal coverage with a term policy from an independent provider. These policies come with set duration limits on coverage and you decide whether to renew once the policy expires.

Remember that whatever life coverage your employer pays for vanishes if you leave that company.

Standard coverage in this category usually pays 60% to 66% of your compensation if you become disabled and unable to work.

As this coverage often comes with a cap, if you are highly compensated, this insurance might also fall short to sustain your standard of living. Estimate your minimum to live on if you become unable to work and, if that number scares you, consider purchasing a supplemental policy.

This pays for assisted living, a nursing home or in-home care late in your life.

Even as our lifespans increase, long-term care premiums escalate. If your employer offers any coverage at a relatively inexpensive group rate, consider locking in some protection. Financial advisors normally recommend LTCI when you turn age 50 – getting it while you are young and healthy under an employer plan may still make sense.

This savings account reduces your taxable income and funds medical co-pays, orthodontist appointments and prescription drug orders, among other expenses.

Figure your out-of-pocket medical costs and sign up to set aside that amount, up to $3,550, pre-tax in an FSA and $7,100 for families. Remember that if you participate in an HDHP, you maintain a related health savings account and can only take advantage of a limited FSA.

Either way, pay for the most of out-of-pocket medical costs with pre-tax dollars.

If you pay for daycare, after-school programs, or summer day camps for children under age 13 or for eldercare for a dependent parent, DCAs help you offset that cost with pre-tax dollars. Again, a working couple can set aside up to $5,000 from paychecks.

When describing the confluence of this year’s events it has become cliché, if not a major understatement, to describe 2020 as a year of uncertainty. Just some of the obvious contributors: COVID-19 and the politicization of lockdown policies. Add to that social unrest from peaceful protests to raging riots. And then there is the virtual firestorm of politics ahead of the elections, to say nothing of the actual firestorms raging across the Pacific Northwest. So how can we be prepared in times of uncertainty?

With so much uncertainty it may be hard for individuals, families, or businesses to know how to plan for next month, let alone plan for the distant future. For many, comfort is found by having certainty in the big three of faith, family, and finances.

Even for the non-religious among us, feeling certain about the future still requires having a degree of faith. We tend to operate from the belief that life will still operate within some band of "normalcy" even if there is some change. That is, we presume that the basics of our governmental, social, and economic norms will at least resemble something similar to today.

Yes, we know that there will be changes in the future, but it is one thing to speculate about taxes and inflation, and it’s another thing entirely to speculate about fundamental shifts like moving from capitalism to socialism. That is a drastic example to make a point.

Perhaps more illustrative is thinking about the fact that the 401(k) has only been around since 1978. What has today become the predominant individual retirement vehicle has existed for less time than most retirees. You can read a brief history of the 401(k) here, and see how it has evolved pretty significantly over the past 42 years.

The good news? It is possible to plan and feel prepared for the future even in the face of uncertainty. Good advice can cut through the chaos and provide some certainty. Especially when the underlying principles are solid regardless of future outcomes.

For example, one never knows when a natural disaster might happen. But, having an escape plan, emergency kits of food, water, clothing, and cash is still good advice even if disaster never strikes. Just being prepared can bring some peace of mind.

This month Strong Valley Wealth & Pension is kicking off a new initiative to help clients not only be more prepared but feel more prepared. Our goal is to help clients gain some additional peace of mind. We believe one way to do that is by reducing the stress of unpredictability in their financial portfolios.

We are implementing an additional tool called Riskalyze. Riskalyze was built on a Nobel-prize winning framework and it helps people better understand risk. This is a scientific and quantitative approach to analyzing risk at both a personal and portfolio level. The tool provides many advantages, but at its simplest level, it can help determine your personal risk score.

Understanding risk is important because avoiding too much risk can affect your goals as negatively as taking on too much risk. Going through the Riskalyze assessment and determining your risk score can help with proper planning.

It is important to note that understanding your risk score can be useful on its own. However, a risk score is designed to be just one of the multiple inputs that shape an individual client's wealth plan.

Strong Valley combines risk scores with experience, training, disciplined investment strategies, and financial principles. This combined approach can help clients be more prepared for planned and unplanned market (or life) changes.

A risk score is a great quantitative measure. However, it does not replace the qualitative factors that come from our focus on having in-depth client relationships. The technical data helps us define and better communicate planning and performance. But there is no substitute for measuring the "real life" factors that impact our clients.

The great news is that Riskalyze can be started on your own online at any time. We can also schedule a time to walk through it together. (You can schedule an appointment here.) Here is some of what you can gain by going through the process:

If you are an existing client and have not done so yet, here is the link to start your Riskalyze assessment, and we’re excited to hear your feedback after going through the process.

We cannot emphasize enough that despite using cutting-edge technology, a risk score does not replace the human aspects of wealth management and retirement planning. This is just one tool that we can use to further refine the strategies and advice we provide. Knowing you is far more important than just knowing your risk score alone.

That said, we think it is such an important tool, that we would highly encourage sharing the link below with your friends and family. There is no obligation to follow-up with a Strong Valley advisor. Of course, we certainly appreciate that most of our referrals come from existing clients.

Every four years, Washington D.C. and Wall Street converge as Americans elect a president and Wall Street tries to figure out what the outcome means for the stock and bond markets. And since so many hypotheses on this topic abound, it’s hard to keep track of them all.

For example, there are those who swear that Wall Street performs better when:

But what if we ranked the best and worst presidents simply by the performance of the stock market? Surely that would settle the debate as to which president was best for investors, right? Well, while it sounds easy – and the editors at Kiplinger did rank presidents from worst to best according to the stock market – there are a few big caveats to consider.

Caveat #1: Since the Office of the President was established in 1789, America has had 44 different presidents. And just three years later, Wall Street was officially founded on May 17, 1792 with the signing of the Buttonwood Agreement. But for the most part,

there really was no “stock market” until the late 1800s, meaning it doesn’t make sense to include the first 22 presidents. So this analysis starts with the election of 1888.

Caveat #2. The Dow Jones Industrial Average was first published on May 26, 1896 and it followed the 12 largest companies in each sector. Today, it tracks 30 companies. The other very commonly-used index – the S&P 500 – although introduced in 1957 it does track data back to the late 1920s. The editors of Kiplinger decided to use the S&P 500 from President Hoover to the present and the DJIA for earlier.

Caveat #3. Returns do not include dividends. Over the last few decades, dividends have become a smaller component of total returns, so not including dividends will tend to favor more recent presidents.

Caveat #4. Data is not adjusted for inflation. This will tend to help presidents of inflationary times (Carter and Ford) and hurt presidents of deflationary times (Hoover and Bush).

Final Caveat. This one is sure to spark heated debate, but it seems fair to not include President Trump on this list simply because his presidency is still going.

#1 of 22

President Herbert Hoover, Republican

Is it any surprise that President Hoover, who took office just a few months before the Stock Market Crash of 1929 that led to the worst bear market in history, would be the worst in terms of stock market performance? It’s not bad enough that Hoover presided over an annualized compound loss of 30.8%, but the cumulative loss of 77.1% is astoundingly awful.

After his landslide win in 1928, Hoover said in his inaugural address that: “I have no fears for the future of our country. It is bright with hope.”

Then just seven months later, on October 24, 1929, the world witnessed the beginning of the Stock Market Crash of 1929, which brought Black Monday, when the DJIA dropped 13% in a single day.

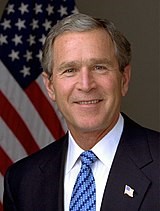

#2 of 22

President George W. Bush, Republican

George W. Bush did not come into office after the Stock Market Crash of 1929 and the Great Depression, but he did come into office after the Dot.com boom of the 1990s and presided during the September 11th terrorist attacks, the Iraq War and the 2008 mortgage crisis.

While there were some good years from 2003 through 2007, many might remember when Bush visited the New York Stock Exchange on January 31, 2007 and gave a speech deriding excessive executive compensation.

Little did anyone know at the time that in less than a year, investors would experience one of the worst bear markets in history stretching from October 2007 through March 2009 when the S&P 500, DJIA and NASDAQ all lost more than 50%.

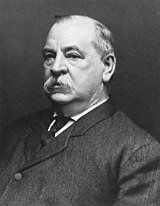

#3 of 22

President Grover Cleveland, Democrat

Stephen Grover Cleveland was the 22nd and 24th president of the United States, the only president in history to serve two non-consecutive terms in office (1885 – 1889 and 1893 – 1897). But his second presidency will be remembered for the third worst in history, measured by stock market performance.

Cleveland’s second presidential term coincided with the Panic of 1893 that ran through 1897 – the end of Cleveland’s presidency. The Panic of 1893 began with a railroad bankruptcy in February 1893 and resulted in over 500 banks closing, more than 15,000 business failing and unemployment hitting 19%.

The deep recession that followed hammered the banking system and by many accounts led to the realignment of the Democratic Party and the beginning of the Progressive Era.

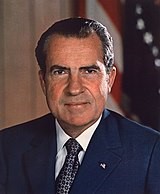

#4 of 22

President Richard Nixon, Republican

President Nixon is remembered for Watergate, his resignation and the Vietnam War, but stock markets performed poorly during Nixon’s presidency too. And while losses of 3.9% a year are bad, if you factor in high inflation, then the performance looks even worse.

In addition to poor stock market performance, Nixon is also remembered for abandoning the gold standard – which meant that the U.S. would no longer convert dollars to gold at a fixed value.

Essentially killing the Bretton Woods system established in 1958, Nixon implemented a series of economic measures – now called the Nixon Shock – to help combat rising inflation. The result was even higher inflation in the 1970s and one of the worst bear markets in history from 1973 – 1974. In fact, the period from January 1973 through December 1974 saw the DJIA lose about 45% of its value.

Next week will bring Part II – and the list might surprise you.