Call Our Office

(559) 384-2900 | Fresno

(619) 480-1413 | San Diego

(619) 480-1413 | San Diego

Your Money

Your Life

Your Way

You are now leaving the Strong Valley Wealth & Pension, LLC ("Strong Valley") website. By clicking on the "Schwab Alliance Access" link below you will be entering the Charles Schwab & Co., Inc. (“Schwab”) Website. Schwab is a registered broker-dealer, and is not affiliated with Strong Valley or any advisor(s) whose name(s) appears on this Website. Strong Valley is/are independently owned and operated. Schwab neither endorses nor recommends Strong Valley. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Strong Valley under which Schwab provides Strong Valley with services related to your account. Schwab does not review the Strong Valley website(s), and makes no representation regarding the content of the Website(s). The information contained in the Strong Valley website should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.

Market swings often prompt investors to reassess their portfolios. To evaluate the efficacy of investments in light of financial goals, it’s important to revisit two key principles—asset allocation and diversification. Any long-term investment plan will most likely have to weather market “ups” and “downs.” Softer markets often create opportunities for purchasing shares at lower prices, and through dollar cost averaging, investors may be able to average a lower cost per share over time. Maintaining a regular investment program and balancing portfolios to account for a comfortable risk level are important to the overall success of financial strategies.

The main objective of asset allocation is to match the investment characteristics of the various asset categories (equities, bonds, cash, etc.,) to the most important aspects of the personal investment profile—that is, risk tolerance, returns and liquidity needs, and the time horizon. Asset categories generally react differently to economic fluctuations.

If an investor assembles assets without careful planning, then they won’t likely know the extent to which the investments are (or are not) consistent with the overall objectives. Since various investment categories have unique characteristics, they rarely rise or fall at the same time. Consequently, combining different asset classes can help reduce risk and improve a portfolio’s overall return. While there is no set formula for asset allocation, guidelines can help to accomplish certain goals (for example, the need for growth in order to offset the erosion of purchasing power caused by inflation).

Diversification is an investment strategy used to manage risk for the overall portfolio, using techniques such as mixing holdings to include a variety of stocks (small-cap, mid-cap, and large-cap), mutual funds, international investments, bonds (short- and long-term), and cash. By varying investments, diversification attempts to minimize the effects that a decline in a single holding may have on the entire portfolio.

To maintain a regular investment program, many investors make dollar cost averaging an integral part of their overall savings plan. Using this systematic investing technique, an investor spends the same amount each period on the asset, but due to market trends, the money buys more shares when prices are low, and fewer shares when prices are high. This may result in a lower average cost per share than purchasing a constant number of shares at the same periodic intervals or if making a one-time large investment.

Dollar cost averaging cannot guarantee a profit or a lower cost per share, nor can it protect against a loss. However, it is a strategy that reinforces the discipline of regular investing and offers a systematic alternative to “market timing.” In order to take full advantage of dollar cost averaging, the investor needs to consider continuing purchases through periods of market down-turns. Periods of falling prices are a natural part of investing, as are strong market intervals. It is important to regularly review the portfolio and meet with a financial professional to help ensure the investment strategies remain aligned with the overall financial objectives.

Life can present some serious storms, and when it comes to financial liability, standard homeowner's insurance might feel as inadequate as a raincoat during a hurricane. That’s where umbrella insurance policies offer an additional layer of protection, when life’s little showers turn into a financial downpour. Umbrella policies are designed to help safeguard a property owner’s income, assets, lifestyle, and legacy, if someone is injured on the property or by a member of the household.

Understanding this protection requires a closer examination of the potential storm clouds and the valuable assets that may be at risk.

Determine the Right Amount of Coverage

Take an inventory of potential risks around the property.

How much coverage is really needed?

A widely accepted guideline is to correlate potential umbrella insurance coverage to the obvious assets, including:

Coverage Guidelines Based on Financial Profile

Consider net worth and potential risks when determining coverage.

A Proactive Approach

Keep in mind that umbrella policies typically require certain minimum limits on underlying home and auto insurance. Be sure to review those policies, as they can provide a significant foundation for an umbrella policy.

Be proactive, don't wait for the storm clouds to gather. A well-chosen umbrella policy may help weather an unexpected financial downpour. Let’s discuss your circumstances and tailor a solution that provides the clarity you deserve.

In 2025, diversification helps with stock market volatility, and April saw the volatility index rise to its highest point since the pandemic. We also look at alternative strategies, bond performance, and scenarios surrounding interest rate cuts later in the year.

Some of life’s biggest moments come with celebration - like selling a business, welcoming a child, or retiring after decades of work. Others arrive quietly, like taking care of aging parents or handling a financial windfall you didn’t expect.

And sometimes, life just throws a curveball.

In moments like these, the question isn’t just, “What’s next?” It’s, “Am I ready?”

Here are just a few of life’s moments that may deserve a fresh financial conversation and a new perspective:

Selling a home or buying a new one

Caring for aging parents or an ill loved one

Getting married or divorced

Starting a business or stepping away from one

Having a baby, adopting, or planning for college

Receiving an inheritance or settlement

Preparing to retire - or realizing you’re not ready yet

Each of these events can reshape your financial picture. The earlier you plan, the more options you have, and the less overwhelmed you’ll feel when the time comes.

We’re here to guide you through life’s most meaningful and difficult moments. Whether you’re planning ahead or facing a new normal, we’ll help you navigate with clarity and confidence.

If something on this list resonates with your current life season, simply reach out to us and we can set up a time to talk.

Each year, the back-to-school season brings a mix of excitement and anxiety for families across the United States. As students prepare to return to the classroom, parents and grandparents face the growing financial burden associated with back-to-school shopping and the rising costs of education. Let’s explore the factors contributing to these rising costs and how families can strategically plan for the future, particularly by leveraging the benefits of 529 plans.

The cost of back-to-school shopping has surged, driven by several factors, including inflation, increased demand for technology, and supply chain disruptions. According to the National Retail Federation (NRF), families with children in elementary through high school are expected to spend an average of $890 on school supplies, a significant increase from previous years. For college students, the average spending can surpass $1,200 when factoring in textbooks, electronics, and dorm supplies.

One major contributor to this rise is the increasing reliance on technology in education. Laptops, tablets, and other electronic devices are now essential tools for learning, especially in the wake of the COVID-19 pandemic, which accelerated the adoption of digital learning platforms.

Another factor is the ongoing supply chain challenges that have led to higher prices for many goods. From shipping delays to shortages of raw materials, these disruptions have created a ripple effect, driving up the cost of everything.

While the cost of school supplies is a significant concern, it pales in comparison to the cost of education itself. Over the past few decades, tuition fees at both public and private institutions have outpaced inflation and wage growth. According to the College Board, the average cost of tuition and fees for the 2023-2024 academic year was more than $10,000 for in-state students at public four-year institutions, more than $27,000 for out-of-state students, and more than $38,000 for students at private nonprofit four-year colleges.

These figures do not include additional expenses such as room and board, textbooks, and personal expenses. As a result, many families are grappling with how to afford a college education without incurring significant debt.

Given the rising costs, it is essential for families to plan ahead. One of the most effective ways to do this is by investing in a 529 plan, a tax-advantaged savings plan designed to encourage saving for future education expenses.

529 plans offer several key benefits that make them an attractive option for parents and grandparents looking to mitigate the financial strain of education:

To make the most of a 529 plan, parents and grandparents should consider the following strategies:

The rising costs of back-to-school shopping and education present significant challenges for families. However, with careful planning and the strategic use of tools like 529 plans, parents and grandparents can better prepare for these expenses.

By starting early, making regular contributions, and taking advantage of tax benefits, families can build a solid financial foundation that supports their children’s educational journey without undue financial strain. In an era where education is more important than ever, a proactive approach to saving and investing is essential for ensuring future success.

A typical college degree is worth a lot of money over the length of a career. A typical degree – but not every college.

College costs rose roughly 7% annually over the past 50 years, about double the average yearly inflation rate. And overall costs of some, including even community colleges, have increased faster than that in recent years, according to the College Board.

In general, higher education does boost lifetime earning potential. Some schools simply seem not worth the investment, though.

To calculate whether a college is worth the investment, use an opportunity cost measure called return on investment (ROI). After factoring all the net college costs, compare 30 years of estimated income of a college graduate versus 34 years of income from a high school graduate who started working immediately and didn’t pay college expenses or assume the debt of student loans.

Future college students (and their parents) must realize that not all colleges are equal. Graduates from the lowest-ranking schools often earn less income after graduation. One can also assume that low-performing schools tend to offer less financial assistance, which leaves graduates with larger debt burdens.

The most highly endowed colleges can reduce their cost of attendance with grants and scholarships. For example, Stanford ranks as one of the most expensive schools based on sticker price. But generous financial assistance makes for a very competitive net cost and would give the school a high ROI score.

Debt burdens are also relative. A doctor’s salary more quickly pays off a high-price education loan than a teacher’s. Good rule: Avoid incurring college debt exceeding half of the expected annual income. Limiting loans in this way allows students to pay off the debt after five years, using 10% of their future salary.

Clearly, an ROI analysis will show a world of difference between the outcomes of graduates of highly rated schools and those graduates of schools near the bottom of the barrel. Attending a college with a poor ROI is not necessarily a mistake, but the financial aid package should be sweet. As with any investment, do the homework before committing time and money to determine if the overall investment is worth it.

The first quarter of 2025 was very different from 2024, with international equities leading the way. How are the US “Mag 7” expected to perform going forward? Let’s take a look! In other news, is it a good time to buy? Finally, stock and bond correlations are changing.

Often, large public companies have teams of people dedicated to reporting organizational changes to the business community and credit rating agencies. Smaller private companies, however, must make more of an effort to ensure that their credit reports accurately reflect the current state of their businesses. They need to make certain that reports are free of errors or omissions that could damage their reputation or hinder access to loans or other forms of credit.

Just as individuals are advised to regularly request and review their credit reports from the major agencies, businesses should also monitor their credit profiles. Like a personal credit rating, a business credit rating provides potential creditors or business partners with a summary of the company’s transaction history. This history is used to determine the level of financial risk the firm represents to the bank or vendor, as well as the likelihood that the business will default on a loan or fail to pay its bills on time.

A good credit rating becomes especially important when a business is seeking to increase its line of credit, attract new investors, to partner with another organization, or sell the company. A strong rating is also useful when the business is making growth-related investments, such as purchasing new equipment, establishing a relationship with a supplier, building inventory, or hosting a promotional event. A credit score influences not only whether a bank approves a loan, or a partnership is formed, but also whether the interest rate and terms of the agreement are favorable to the business.

Information contained in a credit report may be drawn from all organizations with which the company has been involved, including suppliers and creditors. The report will reflect whether the company pays its bills on time or is frequently late in meeting obligations. The report will also show a history of all secured and unsecured loans, working capital, cash flow, sales volume, and overall debt-to-asset ratio. Any liens, collections, or legal judgments against the company will also be included. In addition to fiscal information, a credit reporting agency’s company profile may also include information on the size of the company, employee numbers, major shareholders, business structure, location, history, and reputation.

In developing strategies to maintain or improve a credit rating, start by ensuring that the firm and all employees follow responsible payment procedures. To the greatest extent possible, strive to minimize or effectively manage debt, while increasing assets. Report all information relevant to the business profile, such as ownership or address changes, to the major credit agencies, and check the reports regularly for any errors or omissions. If mistakes or other problems are found, be sure to contact the credit agency to request a correction.

In addition, all information provided to the credit rating agencies immediately becomes publicly available—even to competitors. In some cases, more sensitive data should be withheld from the credit rating agencies, only revealing certain information, on a need-to-know basis, to prospective lenders or business associates.

As the company expands, entrepreneurs should seek to separate their personal credit from their business credit. For example, someone may wish to move from a sole proprietorship or partnership structure to a limited liability company (LLC) structure. Besides enabling owners to separate their business and personal liability, an LLC can also provide certain tax benefits. For more information, consult your tax and legal advisors.

Even so, business owners cannot ignore the health of their personal credit histories, as lenders will often consider the credit scores of all major shareholders during the loan application process. Therefore, maintain a strong personal credit profile, reviewing it regularly and requesting corrections, when necessary. According to the Fair Credit Reporting Act (FCRA), individuals may request a free copy of their credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) annually. For convenience, all three agencies may be accessed through a single website at www.annualcreditreport.com.

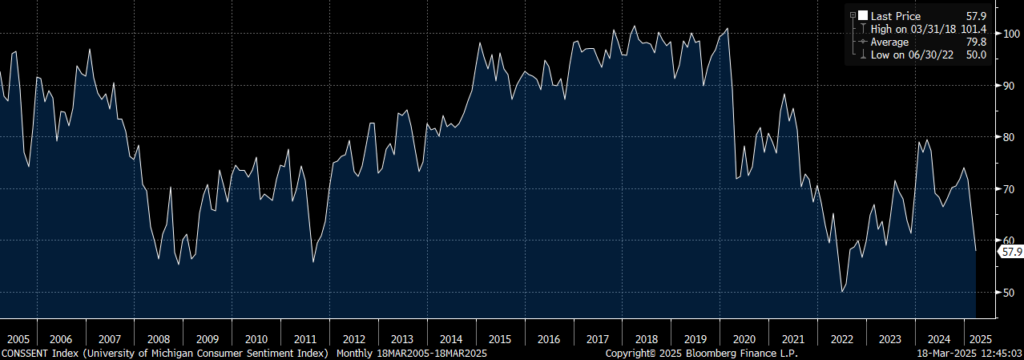

What's your preference, hard or soft? No, not ice cream…data. Economic data, to be more specific. Hard data tends to look at things like GDP, inflation, and durable goods, while soft data looks at surveys of how consumers and investors are feeling. There has been some softening in the most recent hard data related to the U.S. economy. The soft data has declined more, as evidenced by the the Conssent Index, from the University of Michigan Survey of Consumer Sentiment, which has reached recessionary levels.

Conssent Index

University of Michigan

Survey of Consumer Sentiment

The directionality of both types of data confirms an apparent softening in U.S. economic momentum, likely due to the increased uncertainty in the minds of investors and consumers, ahead of tariffs and their potential impact on inflation and earnings. However, the divergence in the magnitude of the two types of data indicates potential opportunities in the market, where sentiment has become too negative relative to the hard data being reported.

The U.S. economy remains stable, with low unemployment and expectations of robust earnings growth in 2025 and beyond. Key to watch going forward will be how the divergence of the two data types converge… soft data improving or hard data deteriorating. Watch for new reports on consumer confidence, as well as the University of Michigan’s consumer sentiment.

Another key data point to consider is the 1-year and 5-10 year inflation expectations from the University of Michigan. There has been a noticeable up-tick in short and longer-term inflation expectations ahead of tariff implementation. Further increases in inflation expectations may make future interest rate cuts more difficult. Simultaneously, bottoms in consumer confidence have historically represented very good buying opportunities in equity markets, as markets appreciate on the back of improving consumer confidence and sentiment.

WHAT HAPPENED

U.S. Rates - The Federal Reserve held rates steady and offered an outlook with slightly higher inflation forecasts and lower growth forecasts in 2025.

U.S. Retail Sales - Retail sales for February came in at 0.2% vs. estimates of 0.6% on a MoM basis, while Retail Sales Ex Autos & Gas came in at 0.5% vs. estimates of 0.4% on a MoM basis.

European Defense – The German parliament approved significant defense spending in support of Ukraine and European defense.

While the Federal government has created several tax-advantaged savings accounts designed to help lower and middle-income workers save for retirement, these plans tend to be less useful for employees earning higher salaries.

Highly compensated individuals who are not currently permitted to contribute directly to Roth IRAs, and younger workers hoping to be in higher tax brackets when they retire, both stand to benefit when companies offer employees the option of contributing after-tax dollars to a type of plan called the “Roth 401(k).”

As the name suggests, the Roth 401(k) incorporates elements of both traditional 401(k) plans and Roth IRAs. Included in the Economic Growth and Tax Relief Reconciliation Act of 2001, the Roth 401(k) allows workers to make Roth IRA-type contributions to 401(k) plans, but without the income restrictions and contribution limits that apply to traditional Roth IRAs.

Although contributions to a Roth IRA are non-deductible, earnings accumulate tax free and qualifying distributions are also tax free. Currently, only taxpayers whose adjusted gross income falls below certain levels are eligible to contribute after-tax dollars directly to a Roth IRA. These income limits do not apply to Roth 401(k)s.

Workers have the opportunity to save more money in the new 401(k) Roth accounts than they could using traditional Roth IRAs. This is because the Roth 401(k) is subject to the more generous limits that apply to conventional 401(k)s.

The Roth 401(k) has other advantages over the Roth IRA. Contributions are made through payroll deductions, rather than through separate arrangements with a bank. Because these plans are administered by employers, contributing to them should be more convenient for workers than opening an IRA. An employee who is currently contributing to a traditional 401(k) plan could, for example, simply opt to have contributions diverted to a Roth version of the same plan.

Lawmakers have stipulated, however, that matching contributions made by employers must be invested in a traditional 401(k), not a Roth account. This means that, even if employees make all of their contributions exclusively to a Roth 401(k) account, they would still owe tax in retirement on withdrawals from funds contributed on a pre-tax basis by their employers.

Workers should also be aware that the 401(k) annual deferral limits apply to all 401(k) contributions, regardless of whether they are made on a pre-tax or after-tax basis. If employees contribute to a Roth 401(k), they may have to reduce or discontinue their contributions to their employer’s conventional 401(k) plan to avoid exceeding these limits. Provided employees comply with these limits, however, they are allowed to put money into both types of 401(k) plans.

In addition, employees considering the Roth 401(k) option should know that RMD (required minimum distributions) will apply to the Roth 401(k), unlike the traditional Roth IRA.

On the other hand, the Roth 401(k) is like the Roth IRA in that investors will not be permitted to withdraw money tax free until they have held the account for at least five years and are at least 59½ years old. The latter provision could make the Roth 401(k) less attractive to employees who are currently approaching retirement.

Talk to your financial advisor to see if the Roth 401(k) might be appropriate for you.