Call Our Office

(559) 384-2900 | Fresno

Your Money

Your Life

Your Way

You are now leaving the Strong Valley Wealth & Pension, LLC ("Strong Valley") website. By clicking on the "Schwab Alliance Access" link below you will be entering the Charles Schwab & Co., Inc. (“Schwab”) Website. Schwab is a registered broker-dealer, and is not affiliated with Strong Valley or any advisor(s) whose name(s) appears on this Website. Strong Valley is/are independently owned and operated. Schwab neither endorses nor recommends Strong Valley. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Strong Valley under which Schwab provides Strong Valley with services related to your account. Schwab does not review the Strong Valley website(s), and makes no representation regarding the content of the Website(s). The information contained in the Strong Valley website should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.

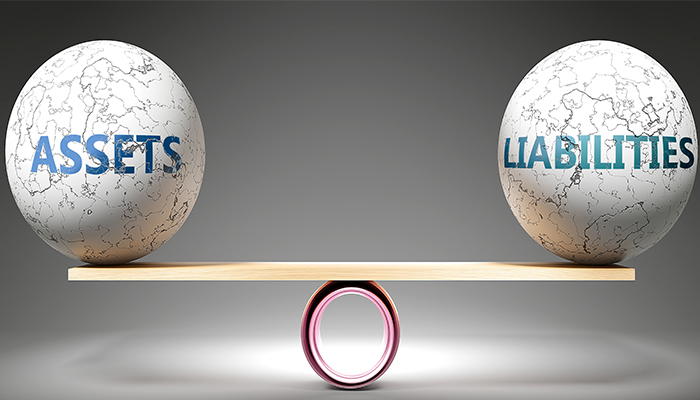

It’s natural for you to gravitate towards the idea of financial planning being focused on growing assets such as stocks, bonds and real estate. Many are surprised to learn that developing a comprehensive financial strategy doesn’t only involve focusing on what you own, but also what you owe.

When the topic of financial planning comes up, most individuals naturally gravitate towards the idea of growing their assets. Stocks, bonds, real estate, and retirement accounts usually dominate these discussions. However, a comprehensive financial strategy doesn't only involve focusing on what you own, but also on what you owe. Liabilities, or the debts one owes, are just as crucial to understand and manage, especially in an economic environment of rising interest rates.

Given the importance of liabilities, here's how one can give them the same attention as assets:

A holistic financial plan is a two-sided coin: assets on one side and liabilities on the other. By valuing liabilities in the same way we value assets, we not only get a clearer picture of our financial health but also make informed decisions that set the stage for long-term financial stability and growth. As interest rates evolve and economic conditions shift, understanding and actively managing liabilities becomes not just a good practice, but a necessity.